Live

Live

QuantFolio

Quantitative portfolio optimization and factor analysis engine — efficient frontier with CML, Max Sharpe / Min Variance / Risk Parity strategies, Monte Carlo simulation, VaR/CVaR, backtesting. Decomposes portfolio returns into Fama-French factors (alpha, market, size, value, profitability, momentum) and classifies performance across bull / bear / high-volatility market regimes.

Live

Live

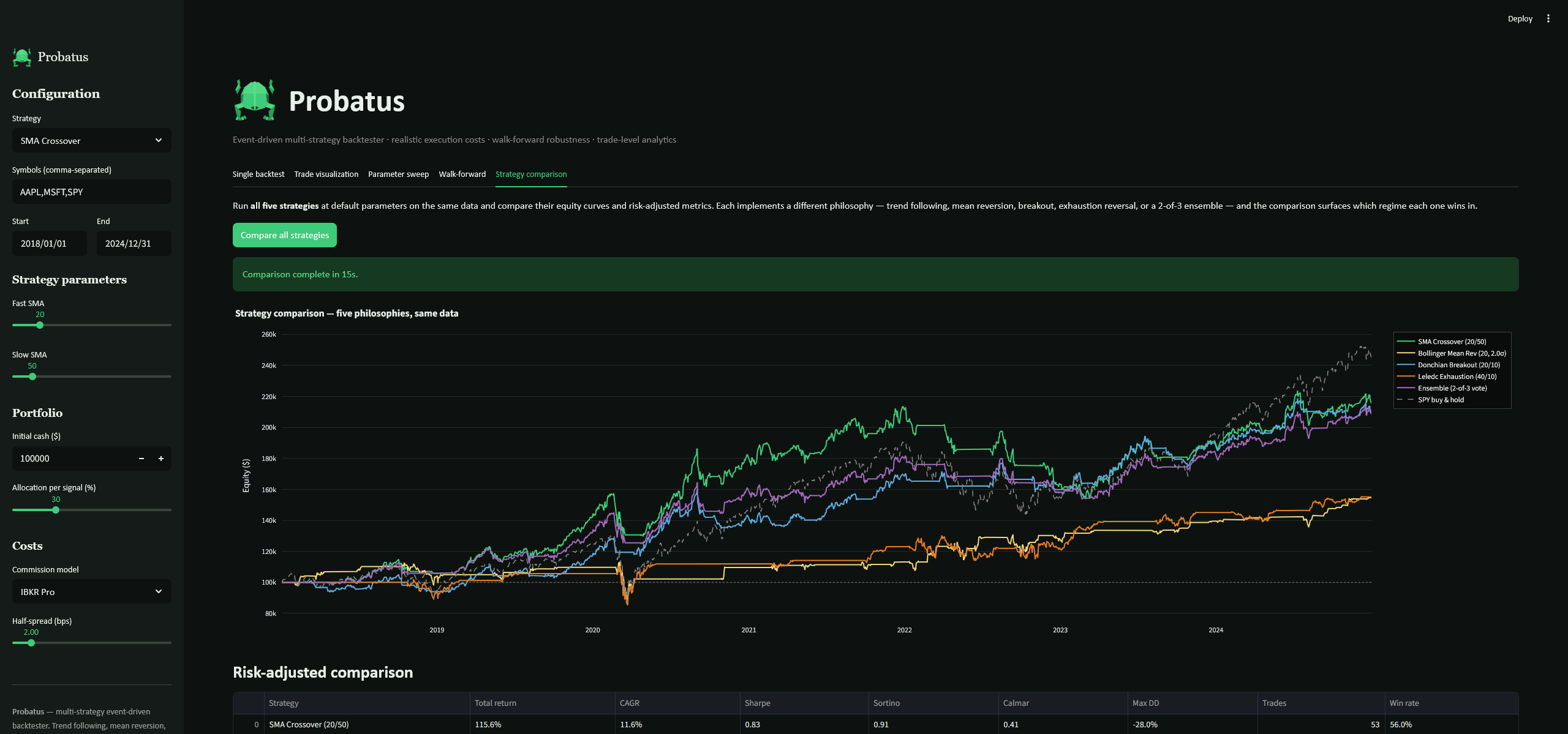

Probatus

Event-driven multi-strategy backtester — five trading philosophies in one engine (trend following, mean reversion, breakout, exhaustion reversal via Pine Script port, and 2-of-3 ensemble) with realistic execution costs (IBKR commissions, bid-ask half-spread, Almgren-Chriss square-root market impact). Walk-forward analysis produces unbiased out-of-sample Sharpe — on AAPL/MSFT/SPY 2018-2024, Donchian Breakout achieves the only Sharpe above SPY (0.98 vs 0.76) while the ensemble produces the smallest max drawdown (-15.4%).

Live

Live

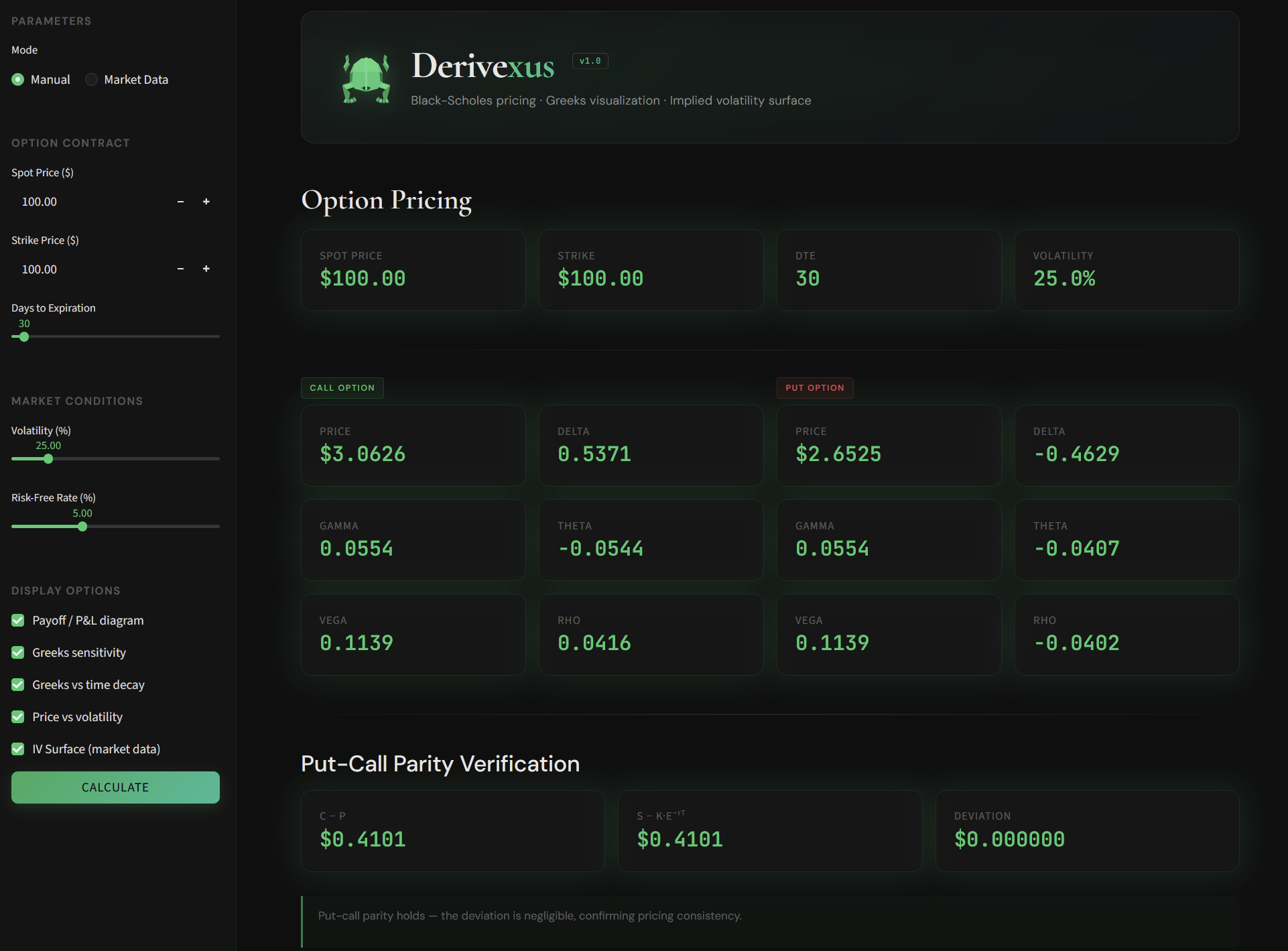

Derivexus

Options pricing and volatility analysis engine — generalized Black-Scholes-Merton with continuous dividend yield, full Greeks suite (Δ, Γ, Θ, ν, ρ), implied volatility surface from live market data. Fits quadratic smile models per expiration and flags contracts whose market IV deviates > 2σ from the fitted smile — a diagnostic for option mispricings.

Live

Live

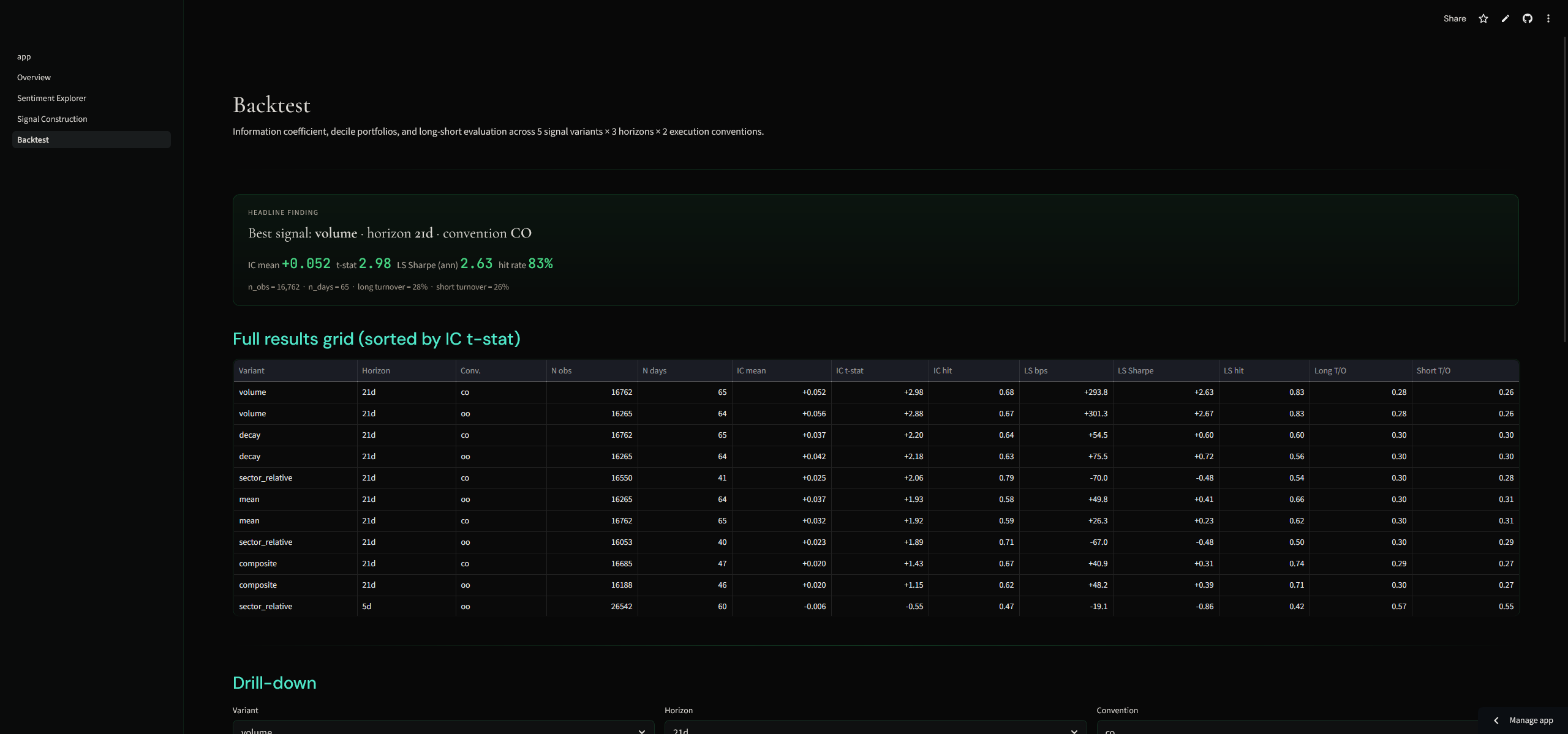

NewsLens

FinBERT sentiment as an equity alpha factor across the S&P 500 — end-to-end research pipeline ingesting ~155k news articles, scoring with a transformer model, and constructing 5 signal variants across 3 forward horizons. Volume-weighted 21d sentiment delivers IC t-stat = +2.98, long-short Sharpe = 2.63 (pre-cost), 83% hit rate over 65 daily portfolios.

Live

Live

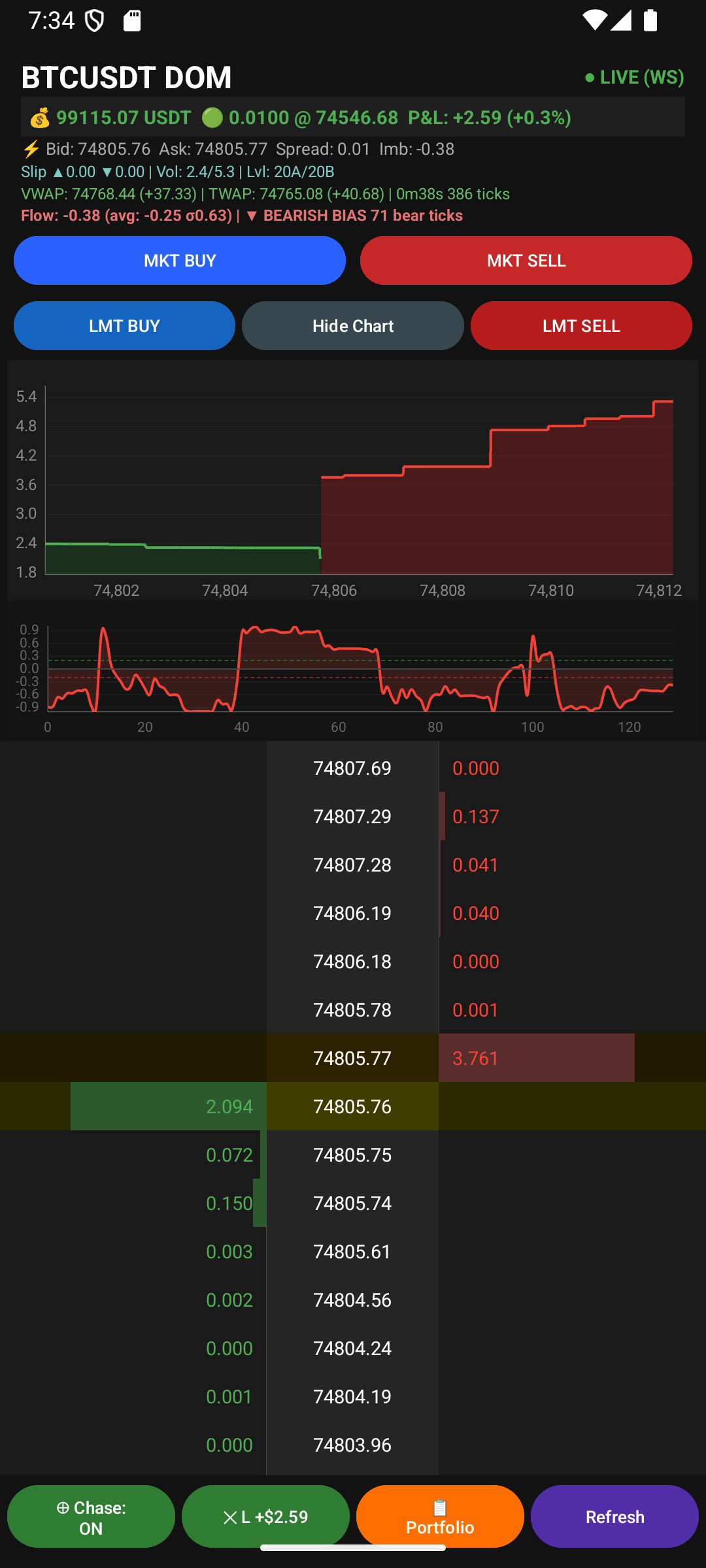

DepthLens

Real-time order book viewer with paper trading, VWAP/TWAP analytics, and order flow imbalance signal detection. WebSocket streaming at 100ms with persistent trade history and live P&L tracking.

Live

Live

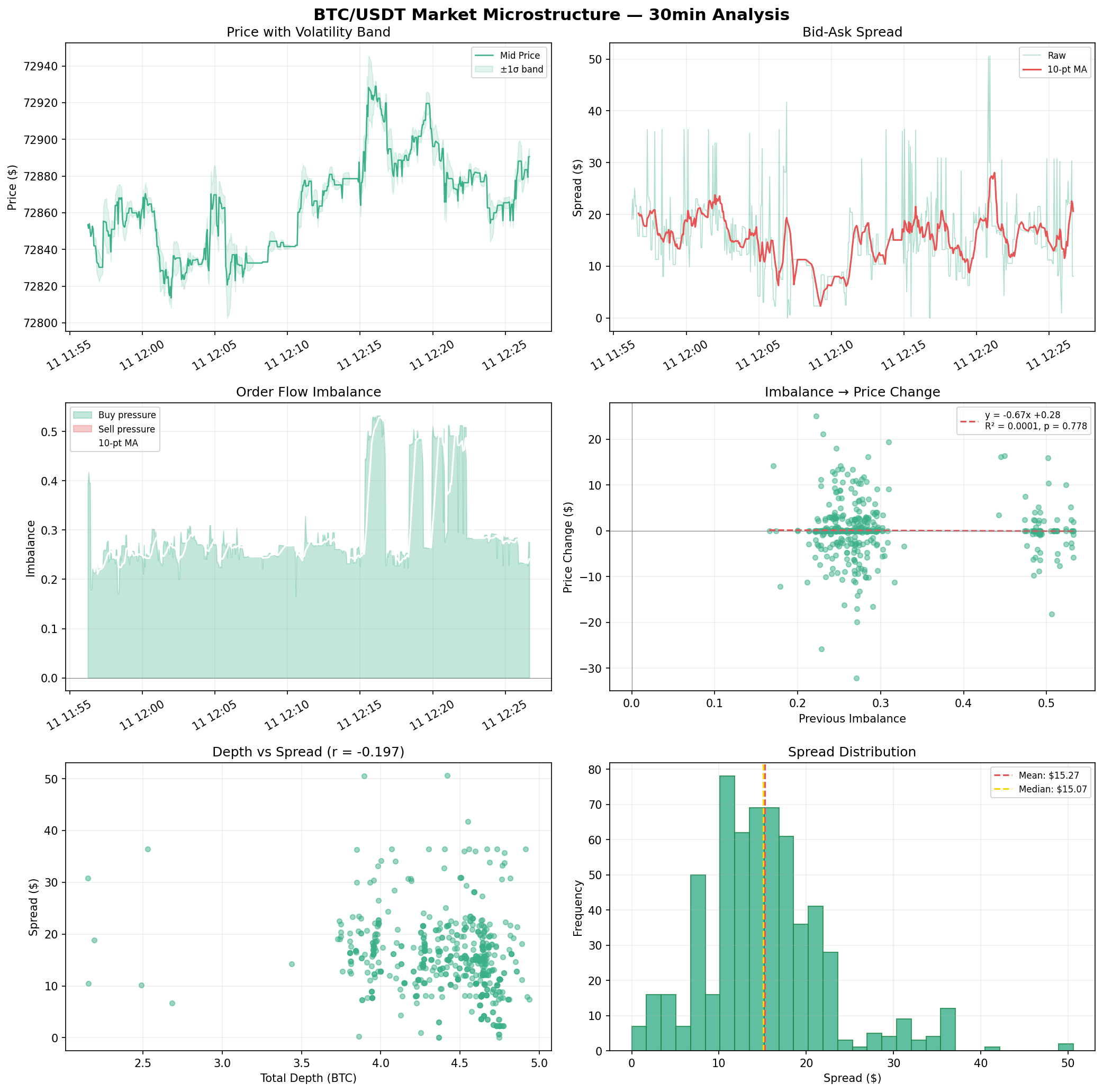

Market Microstructure

BTC/USDT order book analysis — real-time data collection, spread dynamics, order flow imbalance, and statistical regression on 600+ snapshots.